|

6 min read

|

11 Feb 2025

As of 01.01.2018 came into force amendments to the Law "On Taxes and Duties". With said amendments, Latvia has introduced the Organisation for Economic Co-operation and Development (OECD) format of the transfer pricing documentation, consisting of a Master File and a Local File.

Subsequently, transfer pricing documentation requirements apply to Latvian taxpayers (also permanent establishments in Latvia) that enter into transactions with:

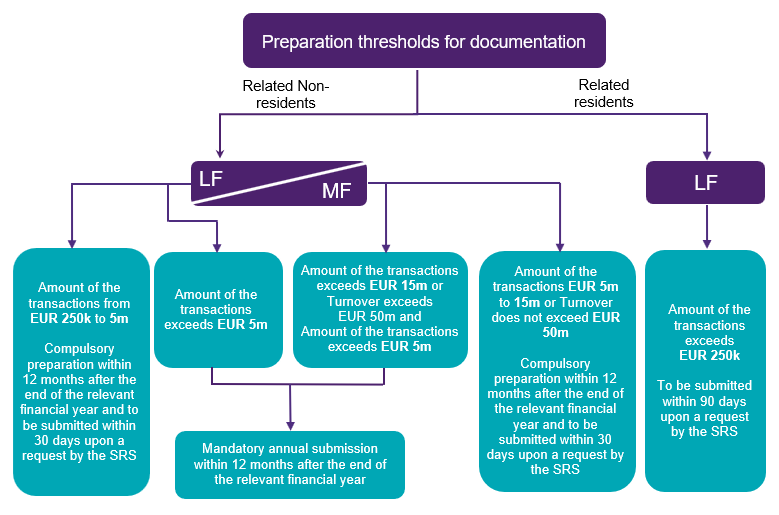

Below are indicated transaction thresholds and submission / preparation deadlines:

The new transfer pricing documentation requirements will no longer apply to taxpayers, who carry out transactions with companies that are exempt from corporate income tax (CIT) or employ CIT rebates. In addition, we would like to draw attention to the fact that if the total sum for a controlled transaction does not exceed EUR 20k, it can be considered as insignificant and information on it does not need to be included in the transfer pricing documentation. However, for transactions conducted between two Latvian taxpayers (with a shareholding above 50%), it remains an obligation to apply the arm’s length price with regard to conditional distribution of profits (in the meaning of CIT law).

The new regulation states that the SRS is entitled to apply a penalty of up to 1% from the controlled transaction amount, but not more than EUR 100k. Said penalty is applicable in cases if the transfer pricing documentation is not submitted within the specified time and if the taxpayer has substantially violated the preparation requirements of transfer pricing documentation. If the documentation is not submitted - the SRS determines the market price of the transaction based on the information at its disposal.

In order to ensure that the applicable transfer pricing documentation and the methodology used are up-to-date, the taxpayer should review the documentation on a yearly basis. If the situation affecting the transfer pricing methodology has not changed significantly, the taxpayer is entitled to review the documentation every three years (except for the comparable financial data included therein).

It is important to note that the amendments state that these requirements are applicable to related party transactions carried out beginning with the 2018 reporting year.

As of January 1, 2018 transfer pricing adjustments trigger CIT obligations, i.e. are included in the CIT taxable base.

The information relevant for the transfer pricing documentation is required to be held for 5 years and the SRS can conduct an audit for an identical period. When starting an audit, the SRS must indicate whether the prices between related parties will be checked against the market prices. When conducting a transfer pricing audit, the SRS may impose a penalty on transactions executed during the last 5 years (except if the SRS has enter into an Advanced Pricing Agreement (APA) with a taxpayer).

In case of any questions, we invite you to contact us.