As of 01.01.2026, amendments to the Law on Taxes and Duties will come into force. Their purpose is to simplify transfer pricing documentation requirements and reduce the administrative burden on taxpayers. The amendments relate to transactions conducted from the reporting year 2025 onwards.

Henceforth, transfer pricing documentation requirements apply to those Latvian taxpayers who engage in transactions with:

· A related foreign company;

· Related legal entities holding at least a 20% participation in the company;

· Related natural persons (in accordance with Section 1, Paragraph 18 of the Law);

· Companies or individuals located in low‑tax or no‑tax countries or territories; and

· Another related Latvian taxpayer, if the transaction takes place within the same supply chain involving another related foreign company or involving companies/individuals located in low‑tax or no‑tax countries or territories.

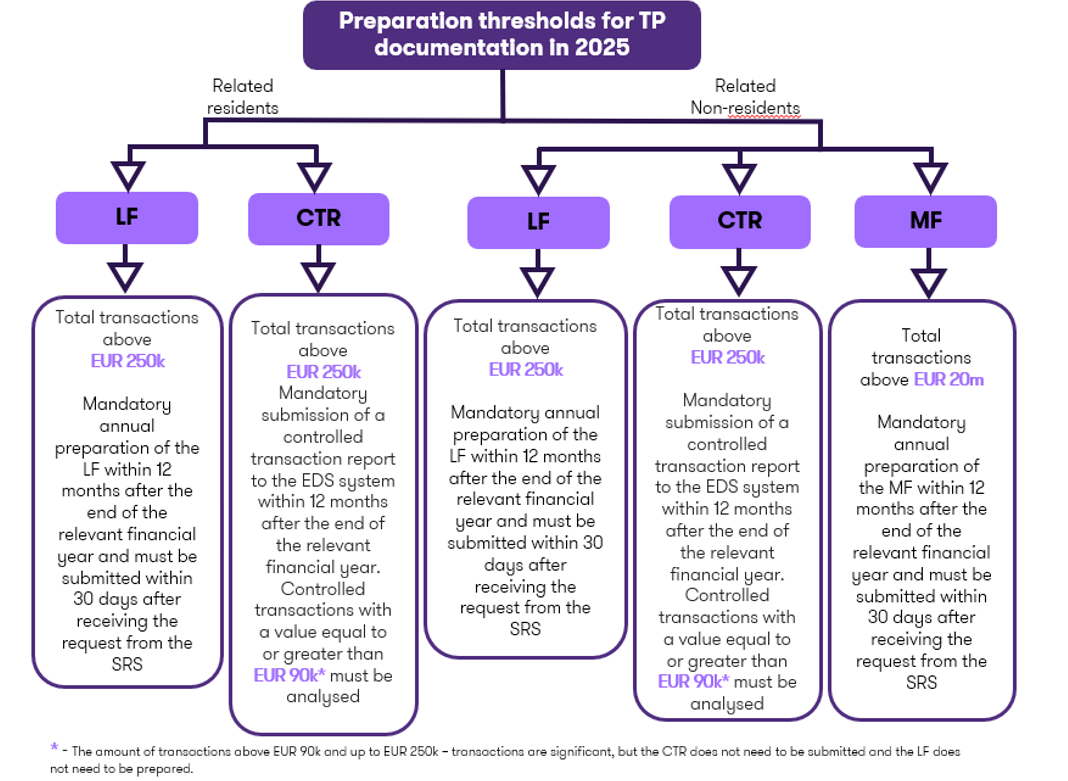

1. Obligations and deadlines (Summary)

![Preparations for TP documentations]()

Documents submitted through the SRS EDS system do not require a signature – they are legally valid.

2. Material Controlled Transaction Thresholds and Definitions

- The threshold for a material controlled transaction has been increased from EUR 20,000 to EUR 90,000.

- Controlled transactions: transactions with related parties (goods, services, loans and interest, guarantees, intellectual property licence fees, management/IT/marketing fees, cost allocations, etc.).

- Related parties: two or more natural or legal persons (excluding capital companies whose participation consists of shares or equity directly owned by the state or a municipality), or a group of such persons bound by an agreement, or representatives of such persons or groups. A detailed description is available in Section 1, Paragraph 18 of the Law “On Taxes and Duties”.

3. Procedure for Updating Financial Data

If circumstances affecting the methodology have not materially changed:

- Transfer pricing analysis (method, comparables) – once every 3 years.

- Financial data (results of the tested party, indicators of comparable companies) – annually.

4. Practical steps for Companies (2025–2026)

- Identify related companies and transaction types (goods, services, financing, intellectual property licence fees, etc.).

- Compile 2025 transactions and calculate total amount with all related companies.

- Assess thresholds:

- Above EUR 250 000 → mandatory submission of a Controlled Transactions Report; local transfer pricing documentation must be prepared.

- Above EUR 20 000 000 → global transfer pricing documentation must also be prepared.

- Prepare methodology (e.g., transactional net margin method (TNMM), comparable uncontrolled price method (CUP), etc.) and the pricing policy.

- Set internal deadlines: submission in the SRS EDS system (12 months) and a 30-day readiness plan for SRS request.

- Ongoing annual maintenance: update financial data and review any material changes in the business.

5. Common risks for beginners

- Failure to calculate the total amount with all related companies.

- Failure to identify “invisible” transactions: interest, guarantees, licence fees, management fees.

- Documentation is prepared only upon request (30 days is insufficient).

- No consistent pricing policy, or the policy is not followed in practice.

6. Short FAQ

Is the Controlled Transactions Report always required?

Yes, if the total amount of controlled transactions with related companies exceeds EUR 250 000.